If It Was Stolen, Data Must Have Value!

If It Was Stolen, Data Must Have Value!

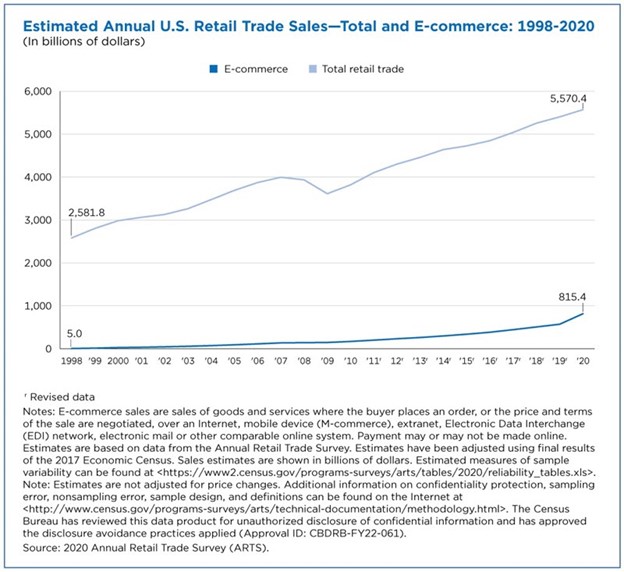

The holiday season brings to mind many things: family, fun, turkey, and of course, shopping. It is no mystery that online shopping continues to increase year over year, as evidenced by the below chart.

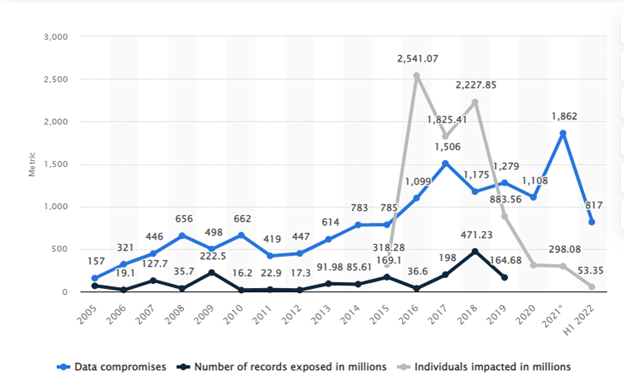

As shoppers move to online purchases, more and more data is floating around the internet. Unsurprisingly, data breaches are also on the rise. The below chart from Statista shows the increase in data breaches over time, the number of records exposed, and the number of individuals impacted. (source)

While the fact that data is stolen would imply that the data has value, not all agree. A judge in Arizona, in Griffey v. Magellan Health Inc., 562 F. Supp. 3d 34, 46 (D. Ariz. 2021), stated “Plaintiffs only identify an illegal market for their personal information, the ‘dark web.’ This Court declines to recognize the “dark web” as a legitimate market by which individuals may sell their information.”

Not only is this view counter to common sense. The rising number of data breaches implies that data does have value. It’s also counter to the opinion of the valuation community.

Data is similar to other intangible assets where value is readily developed using traditional valuation approaches that incorporate growth, profitability, and risk elements. Appraisers need to have a strong understanding of the subject data set’s attributes, but these are common investigative tools in valuations. The traditional valuation approaches include the market, income, and cost approaches using, for example, the multi-period excess method (MPEEM), the with-and-without method, and the relief from royalty method.

The Market Approach

Today, companies are using advanced analytics to more fully understand their data, and to identify ways to license it to third parties. In addition, within various ecosystems, data exchanges are being developed so market participants can aggregate and trade data assets, and participating companies can exchange data to create even more value for their enterprises. As companies continue to mine their data and develop models to transact in this asset category, these transactions can be used to derive market indications of value. (source)

The Cost Approach

A method that uses the concept of replacement cost as an indicator of value. The premise is that an investor would pay no more for an asset than the amount for which the utility of the asset could be replaced, plus a required profit/return to incent a third party to replace the asset. (source)

Multi-Period Excess Earnings Method (MPEEM)

An income approach methodology that measures economic benefits by calculating the cash flow attributable to an asset after deducting “contributory asset charges,” which are appropriate returns for contributory assets used by the business in generating the data asset’s revenue and earnings. (source)

With-and-Without Method

An income approach method for estimating the value of data assets by quantifying the impact on cash flows if the data assets needed to be replaced (assuming all of the other assets required to operate the business are in place and have the same productive capacity). The projected revenues, operating expenses, and cash flows are calculated in scenarios “with” and “without” the data, and the difference between the cash flows in the two scenarios is used to estimate the data’s value. (source)

Relief From Royalty Method

Another income approach method built on the assumption that if the company doesn’t own the data asset, it might be willing to license the data from a hypothetical third party who does. In this method, the company would forgo a certain amount of profitability to license the data from a third party over a certain lifecycle. (source)

Data intuitively has value, regardless of the market it’s sold in, and there are industry-accepted ways to value it. Simply put, Griffey v. Magellan Health Inc. got it wrong on their valuation position. Hopefully, an informed reconsideration by the judge, or perhaps an appeal of the ruling, will ensure that justice is properly served to the plaintiffs.

Questions?

Brady Ware offers a comprehensive range of advisory services, including strategic advisory, financial analysis, tax compliance, litigation support, employee stock ownership plans, succession planning, mergers and acquisitions, quality of earnings analysis, tax structuring, and business valuations. Our team of experienced professionals provides tailored solutions to help clients achieve their financial goals, minimize risks, and optimize their business performance. Brady Ware’s advisory services focus on developing solutions and creating pathways to success for businesses facing complex challenges, leveraging their deep understanding of business operations, transactional situations, and personal and ownership legacies.