Dealership Year-End Tax Planning Guide – DOWNLOAD

Essential 2025 Year-End Tax Strategies for Dealership Owners (LIFO, Depreciation, and OBBBA Updates)

The close of the tax year is a high-stakes period for car dealership owners. Effective year-end tax planning can significantly influence your net income and cash flow, particularly given the unique complexities of inventory valuation, capital expenditures, and specialized vehicle deductions within the automotive industry.

Our guide below outlines three important strategies along with an actionable checklist to help you navigate your 2025 tax obligations and opportunities. Additionally, the One Big Beautiful Bill Act (OBBBA), enacted in July of this year, introduced significant updates for car dealerships.

I. Inventory Management: The LIFO Strategy

Inventory — specifically new vehicle inventory — is the single largest asset for most dealerships, and the method used to value it is the most powerful tax lever you possess.

Last-In, First-Out (LIFO)

Most profitable dealerships utilize LIFO to account for new vehicle inventory. In a period of rising new vehicle costs (inflation), LIFO assumes the most recently purchased (highest cost) vehicles are the first ones sold.

- Tax Advantage: This maximizes your Cost of Goods Sold (COGS), which lowers your reported taxable income. The cumulative tax deferral is recorded as the “LIFO reserve.”

Critical Year-End Action: LIFO Reserve Calculation

A precise, reasonable estimate of your LIFO adjustment for the year must be recorded on all versions of your December financial statement. This is non-negotiable for LIFO compliance.

Used Vehicle Write-Downs (FIFO/Cost)

For used vehicle inventory valued using FIFO (First-In, First-Out) or cost, you have an opportunity to take a tax deduction by writing down the value of any vehicles whose current wholesale market value (as of December 31st) is less than your cost. Documentation is key.

“Inventory—specifically new vehicle inventory—is the single largest asset for most dealerships, and the method used to value it is the most powerful tax lever you possess.”

II. Strategic Capital Investment and Depreciation

The timing of equipment and property purchases is crucial for maximizing immediate tax deductions through accelerated depreciation.

1. Section 179 Expensing

Section 179 allows you to deduct the full cost of qualifying property (new or used equipment, software, service tools, etc.) in the year it is placed in service, up to a maximum limit.

2025 Key Limits:

- Maximum Deduction: Up to $2,500,000.

- Phase-Out Threshold: The deduction begins to phase out once total qualifying purchases exceed $4,000,000, making it primarily a small and medium-sized business incentive.

Heavy SUVs/Trucks Rule

Many SUVs and crossovers with a Gross Vehicle Weight Rating (GVWR) exceeding 6,000 pounds qualify for a special cap, set at $31,300 for the 2025 tax year. Heavy-duty pickup trucks, box trucks, commercial vans, and other vocational/specialized vehicles may qualify as equipment for the 100% immediate expensing.

2. Bonus Depreciation (100%)

The OBBBA permanently reinstated the 100% bonus depreciation deduction for qualified property acquired and placed in service after January 19, 2025.

The Power Combination

You can typically apply the Section 179 deduction first (subject to its income and spending caps), and then apply 100% Bonus Depreciation to the remaining basis of the asset. This often allows for an immediate, 100% write-off of the asset’s purchase price in the first year.

Example: If a service center lift costs $50,000, you can deduct the full $50,000 in 2025, provided it is placed in service by December 31st.

III. Timing of Income and Expenses

Careful management of the timing of income recognition and expense payments can shift taxable income between 2025 and 2026.

| Strategy | Action | Goal |

|---|---|---|

| Keep Journals Open | New Vehicle Purchases: Keep your new vehicle purchase journal open into early January 2026 to ensure all vehicles built and in transit at 12/31/2025 are recorded as purchases in 2025. | Maximize 2025 LIFO deductions and inventory levels. |

| Employee Bonuses | Accrue Expense: Employee bonuses (for non-owners) can be accrued and deducted at year-end as long as they are paid within 2.5 months of year end (by March 15, 2026). | Ensure the expense is captured in the current tax year. |

This comprehensive approach, combining industry-specific accounting rules with general tax acceleration strategies, will position your dealership for a powerful year-end result as well as help structure your 2026 effectively by applying this same approach.

Disclaimer: This article provides general information and should not be considered professional financial or tax advice. Please consult with a qualified CPA or financial advisor for guidance specific to your individual business needs.

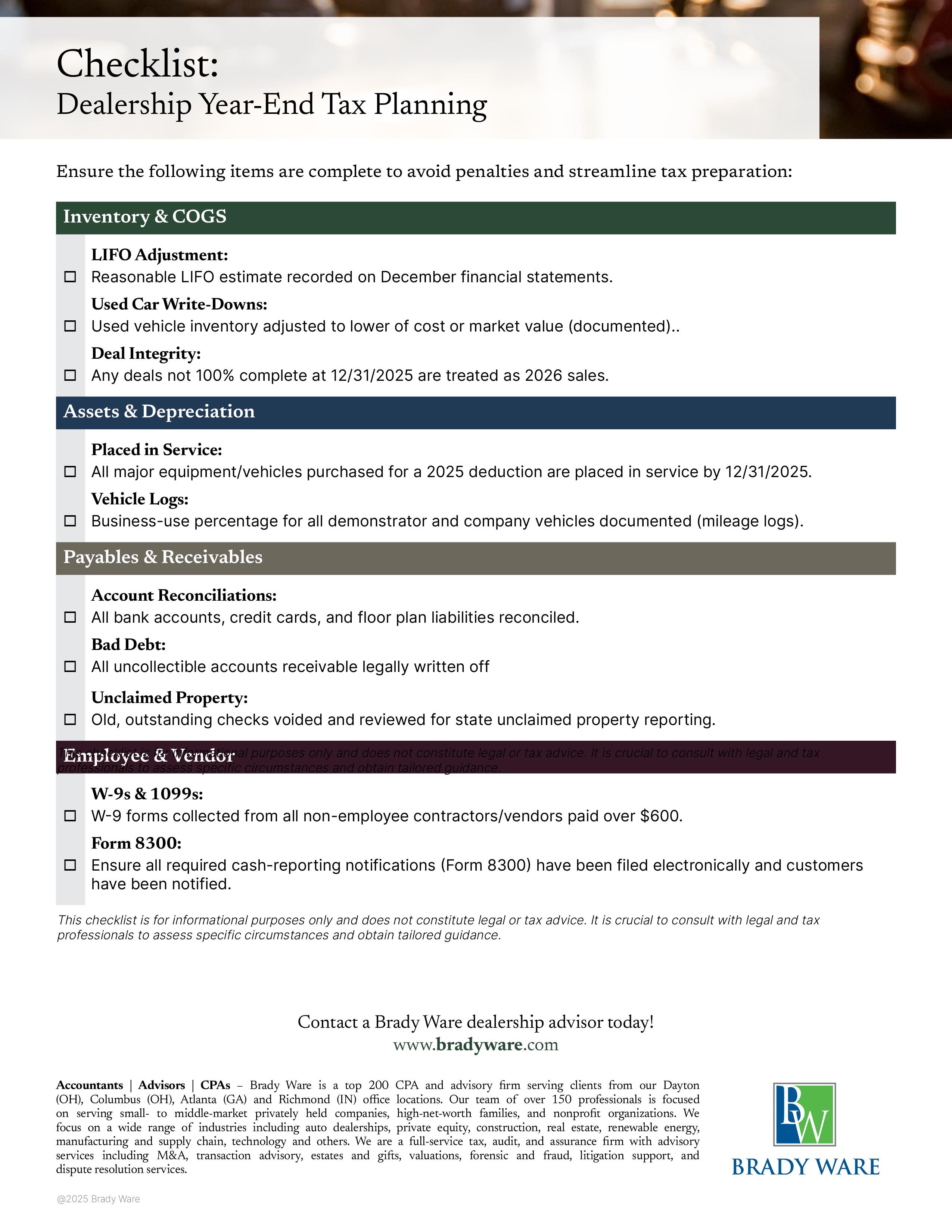

This “Year-End Dealership Tax-Planning Checklist” provides car dealership owners with an actionable, category-based summary of critical tasks, including LIFO adjustments, asset depreciation, and W-9/1099 compliance, that must be completed before year-end to minimize 2025 taxable income and ensure administrative compliance.

Dealership Experts

Kristin Krabacher is a financial strategist with Brady Ware Dealership Advisors, specializing in auto dealer profitability and tax optimization. With over 15 years of experience guiding dealership owners, Kristin excels at translating complex tax laws into clear, actionable insight. She’s helped countless clients enhance gross profit, improve compliance, and make smarter financial decisions through tailored benchmarking and audit-ready processes.